SETTING THE SCENE: A DECADE OF DEMAND, A TERMINAL CONSTRAINT

With the opening of Navi Mumbai International Airport (IATA Code NMI) in December 2025, Mumbai’s aviation market is at an inflection point. BOM handled 55.3 million passengers in FY2026, indicating modest growth of 0.3% year-on-year and a CAGR of 4.6% from FY2011 (29.2 million). However, its competitor hubs grew far more aggressively – BLR clocked an impressive 12% CAGR till the covid pandemic while Delhi grew at 9.5% CAGR on a larger base.

Constrained by dense urban development, BOM operates effectively as a capacity-limited system, with infrastructure designed for ~50 million passengers annually and while incremental capacity has been added in stages since, none of these interventions has represented a material step-change in design capacity. The utilization metrics at Mumbai airport are on steroids but there is a physical limit and for a while the airport has operated a very flat demand profile with very few fire breaks to recover. A schedule without much flexibility can result in significant delays on bad weather days.

The capping of growth at Mumbai over the years has accelerated the redistribution of domestic traffic to alternative hubs. Bengaluru has been the clearest beneficiary as of April 2026, domestic seat capacity at BLR has overtaken that of BOM.

Now with the supply returning (NMI is already India’s ninth busiest domestic airport in terms of daily seats in the summer 26 schedule), it has set the stage for Mumbai’s transition to a dual-airport system, and reworking of the airline networks that have been in place to cater to a single gateway.

THE TRANSITION: NMI ENTERS THE SYSTEM

NMI opened with a plan to augment capacity to handle 20 MPPA in the 2nd year of operations (as per the approved Master Plan). The airline and market response was immediate. By March 2026, NMI was recording 221,586 actual domestic passengers in a month. The BOM/NMI system recorded approximately 3.41 million domestic passengers in March 2026, a 1.8% increase over the same month in the previous year. For the same month, the existing Mumbai airport clocked a lower demand than last year by about 5% suggesting some redistribution of traffic and a slightly larger pie.

The onset of the Summer 26 schedule saw a substantial bump up to the supply partly driven by exogenous circumstances. During the planning stage for Summer 2026, ATC at BOM Airport announced reduction of 80 movements across airlines to reduce airspace congestion owing to safety risks. This led to some airlines scheduling more flights at NMI. This was done taking into account potential air congestion which becomes challenging during bad weather situations. The supply glut due to the external factor has resulted in airlines scheduling 393,819 departing seats for April 2026, just four months after commencement. The demand allocation could change from May 2026 with the recent switchback by ATC[1].

TRAFFIC REDISTRIBUTION: WHO MOVED, WHAT MOVED, AND WHERE

The schedule[2] data for April 2026 shows how the domestic airlines are carving out the supply across the BOM/NMI system. In comparison, GOX enjoyed a market share of 15.4% of the Goa airport system in January 2023 and took over two years to reach the 40% mark.

IndiGo anchors the NMI network with around 400 of the 504 weekly departures, a 74% market share at the new airport. Indigo has redistributed some of its routes to NMI from BOM, thereby dropping its market share at BOM by 3.4% (see footnote below on the reason for the switch). Full Service carrier Air India is yet to open its account at NMI while its wholly owned low-cost subsidiary, Air India Express, operates 49 weekly departures from NMI. Akasa Air operates a similar level of operations at 56 weekly departures at NMI. Air India has chosen to grow its market share at BOM, growing from 754 to 810 weekly departures (+7.4%) and consolidating its full-service carrier identity at the current hub. Low-cost carrier. SpiceJet has expanded aggressively at BOM, up 75% from 84 to 147 weekly departures, but surprisingly has decided not to chase slots at NMI.

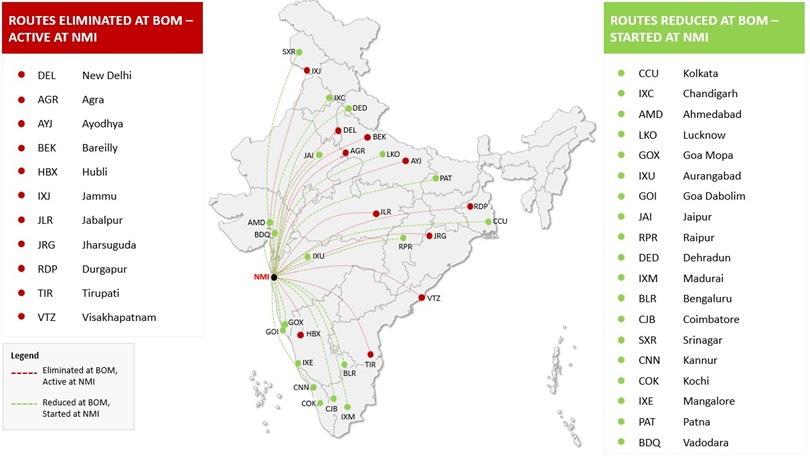

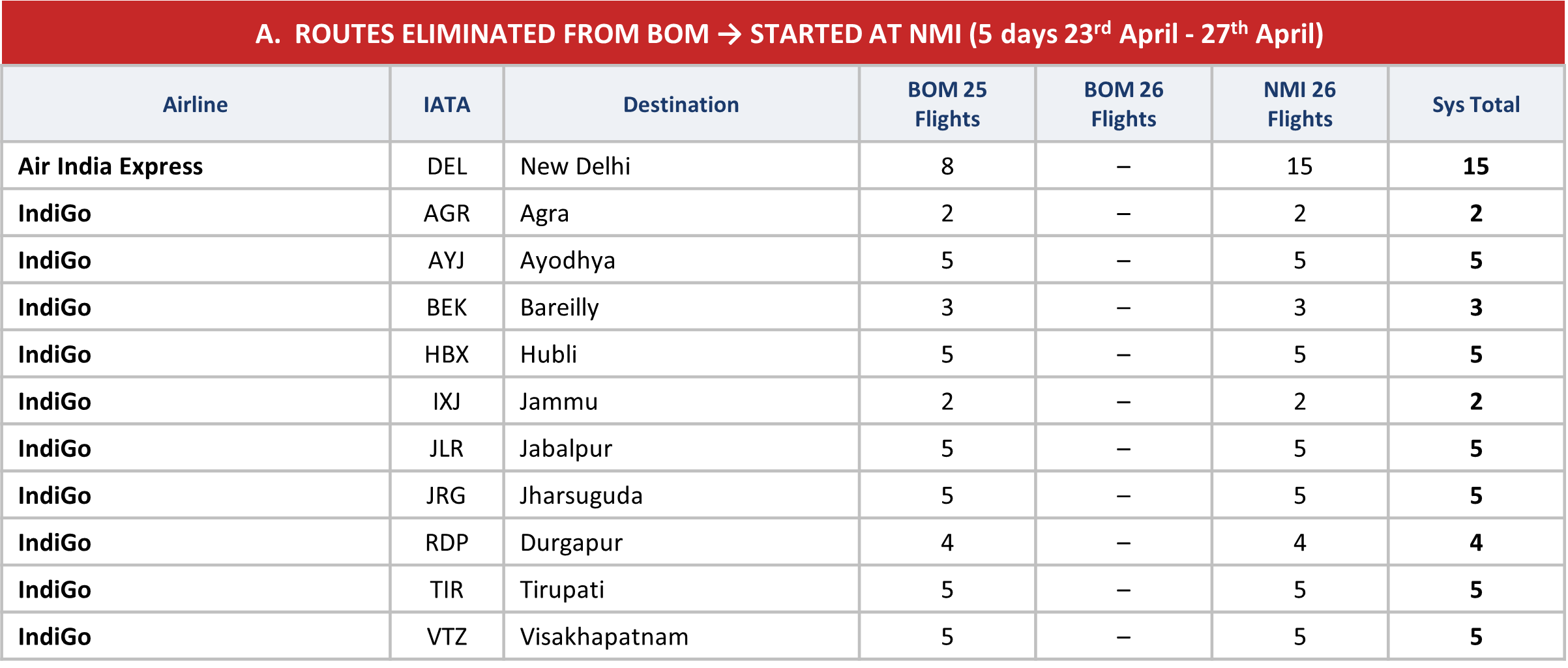

DESTINATION-LEVEL SHIFTS: THE NETWORK EVIDENCE

The route-level data reveals the nature of the shift. Eleven routes by airline have completely moved from BOM to NMI. Some of these are not temporary frequency reductions but deliberate changes of operating base:

Some have been moved to make way for better point to point operations to denser markets from the existing Mumbai airport. This would mean that the NMI will witness a much higher % of Domestic-to-Domestic transfers in the near term, functioning as a consolidation funnel. The implication on the planned infrastructure warrants a reassessment by the airport operator for development of future phases.

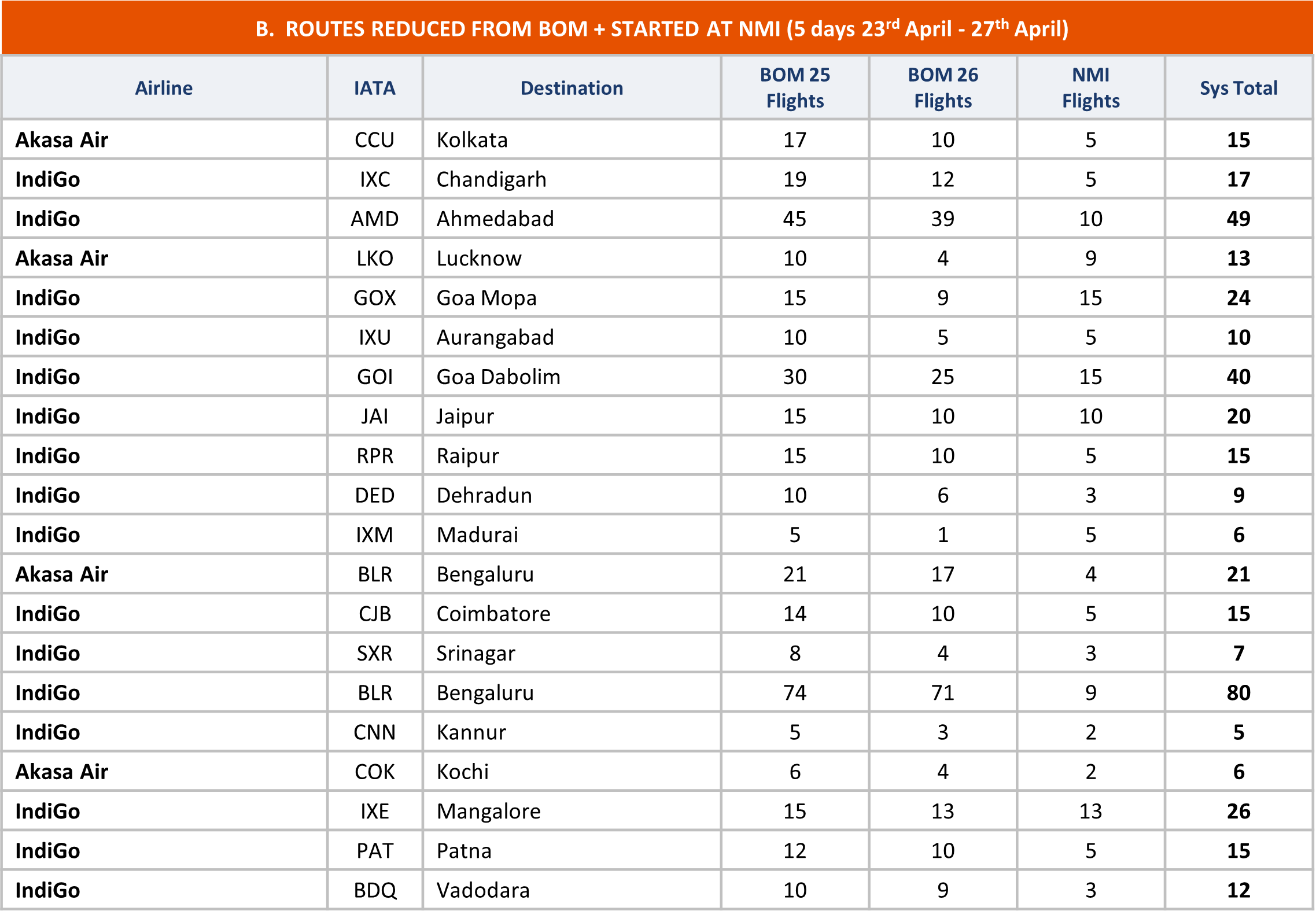

The total service frequency has increased for many routes with new service in NMI being balanced by a drop-in service at BOM.

Air India Express has expanded its footprint and added two routes (that it didn’t serve before from the Mumbai catchment) – Bengaluru and Hyderabad. Similarly, Indigo has started service to Bhavnagar, Diu, Ghaziabad, Belgaum, and Kolhapur – locations which were not served by the airline from BOM in recent times.

RELIEF AIRPORT OR GROWTH DRIVER?

The Goa parallel offers a useful reference point and a cautionary one. When GOX opened in January 2023, the GOI/GOX system grew from 11.16 million to 11.62 million passengers between 2023 and 2025, a 2% CAGR, meaningfully below India’s broader market growth rate of approximately 6.6% CAGR over the same period. System-wide seat supply across both Goa airports grew just 3.6% over two years. The dual-airport framework improved infrastructure quality and competitive positioning, but it did not of itself generate a step-change in demand. Goa’s market was constrained by factors beyond infrastructure such as overtourism dynamics, accommodation cost inflation, and the competitive draw of South-East Asian leisure destinations.

Mumbai market is different. The BOM catchment carries a GDP density and corporate travel base that Goa’s leisure-weighted market does not. The early signs are encouraging that Mumbaikars will finally have a choice at a more reasonable price point. NMI is growing the pie, not just redistributing it. What the data establishes is that NMI is not functioning solely as a relief valve for a capacity-constrained legacy airport.. It is simultaneously operating as a network expansion platform, a second gateway to the Mumbai Metropolitan Region catchment that is enabling connectivity to destinations the legacy airport was never positioned to accommodate.

A key factor to address the “how large is the pie” question is the ownership across the two airports. Many dual-airport systems thrive on friction. Two operators, two sets of commercial incentives, two slot coordinators, each airport competes for the same airlines, the same routes, and the same aeronautical revenue. Goa is the clearest Indian example: AAI at Dabolim and GMR at MOPA spent the first two years of co-existence pulling carriers in opposite directions through competing incentive structures.

Adani Airport Holdings operates both BOM and NMI under a single commercial and operational framework. That distinction matters more than it might appear.

A unified operator can distribute slots, routes, and airline relationships across both airports as a network decision rather than a competitive one. Airlines could potentially deal with a single commercial interface and it can be argued that a single tariff system would be the best outcome (though not an option under the current regulatory regime where BOM’s cash flows are ring fenced from NMI’s). One ground handling agreement, and one slot reallocation conversation. Route migration from BOM to NMI may not require an airline to exit one commercial relationship and enter another; it only requires a scheduling change. The airlines would bear the cost of operating at both airports but this friction point could be resolved through commercial incentives.

The pricing level is equally significant. A single operator can structure differential tariffs, lower landing fees and handling charges at NMI for new routes, LCC operations, and off-peak services. Airlines look at a system wide cost. The allocation strategy is also important. BOM as the premium, slot-constrained, FSC and international hub; NMI as the growth platform for domestic, LCC trunk routes, and scalable new capacity. That is not a strategy two competing operators could coordinate.

IndiGo’s announced expansion plans to 30 new destinations and 400 additional weekly departures from NMI points firmly toward a growth driver rather than a relief-airport holding pattern. It points to NMI aspiring to be the hub/funnel to connect to various tier 2/3 destinations. This has implications for the airport infrastructure currently designed for the 20 MPPA operation. The airport’s 20 MPPA Phase-2 capacity provides ample headroom for this trajectory; the constraint, if any, will be airside slot coordination and transfer facilities.

AVINIA’S VIEW

Some routes that migrate — fully or partially — to NMI are unlikely to return though some switchback to BOM with the ATC restriction being lifted for the rest of the Summer 26 schedule. As NMI’s operational reliability matures and its commercial proposition strengthens, the incentive for carriers to concentrate incremental growth at the newer facility will intensify. Air India’s commitment to BOM and SpiceJet’s aggressive BOM expansion demonstrate that the incumbent hub retains strategic value for full-service and recovering carriers but the window to reposition BOM as the premium FSC and international gateway in the system, while NMI absorbs domestic LCC growth, is open now and will not remain open indefinitely.

The long-term vision for NMI (90 MPPA), with the potential to anchor an aviation-driven urban cluster across Navi Mumbai and the surrounding industrial zones is a real possibility . By the 2030s, Mumbai Metropolitan Region will have airport infrastructure that is finally proportionate to the size of its economy. The planning and investment decisions (Master Plan Update expected) made in the next three to five years will determine whether that infrastructure operates as a coherent, differentiated dual-airport system. With a single operator, the onus is on the operator to align its decision.

The ball has been set in motion for what could be the busiest dual airport system in India (did someone say third runway at NMI) in 10 years.