The Scale of the Opportunity

Air freight carries approximately 35 percent of world trade by value, despite accounting for less than 1 percent of total cargo volume by weight. In an era defined by speed-to-market, supply chain resilience, and the growth of cross-border e-commerce, the sector’s importance continues to compound.

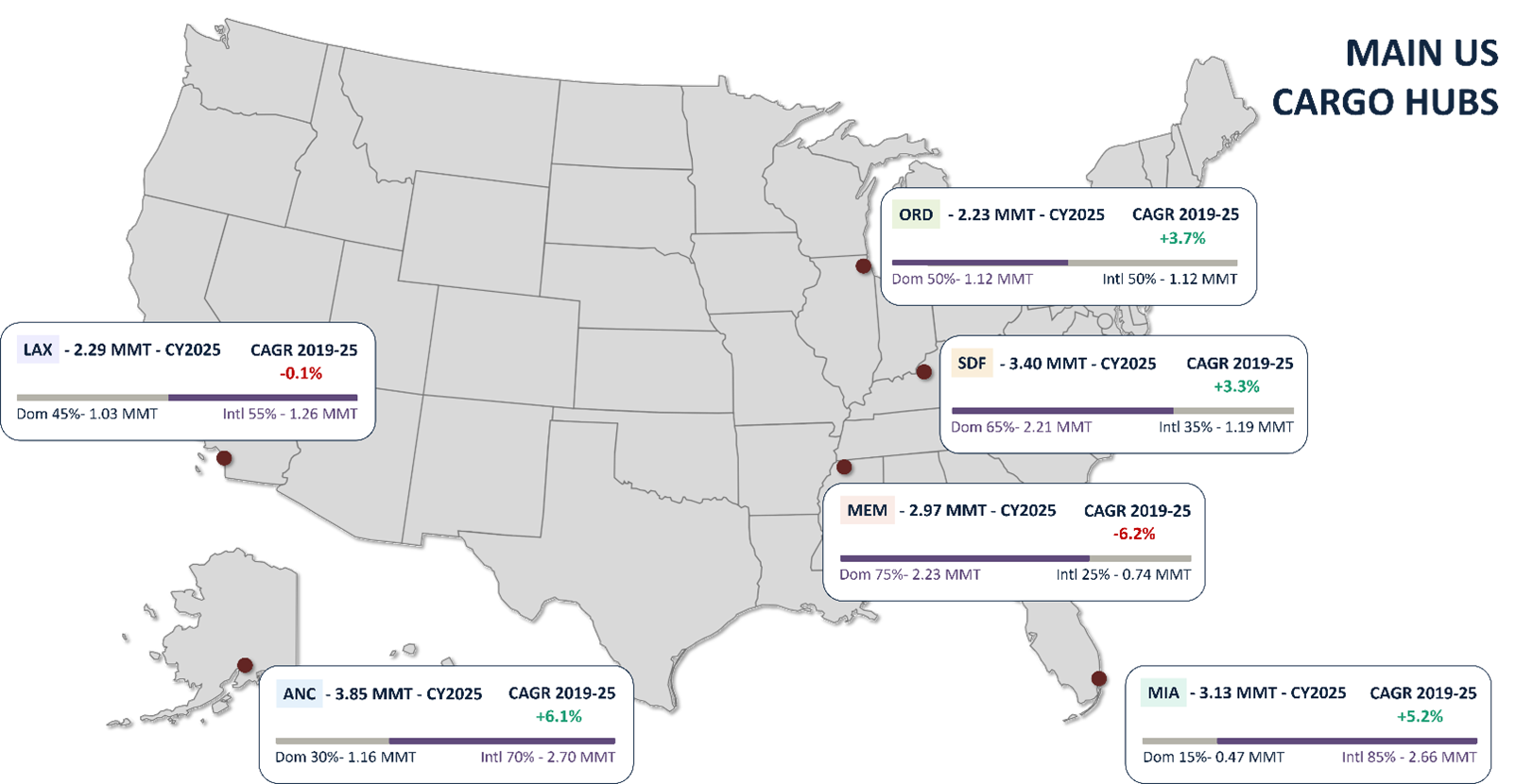

Globally, airport cargo volumes reached a record 128.9 million metric tonnes in 2025 up 2.9 percent year-on-year. Six of the world’s twenty busiest cargo airports are in the United States, and the country hosts three of the top five global express cargo hubs.

Ted Stevens Anchorage International Airport (ANC) now ranks first in the United States and third globally for air cargo throughput, handling approximately 3.9 million metric tonnes and ranking third globally behind Hong Kong and Shanghai Pudong. Its recently completed Master Plan Update – a 20-year development framework projects 2.8 percent compound annual cargo growth and identifies over $300 million in near-term cargo infrastructure investment. UPS’s Louisville Worldport surpassed FedEx Memphis to become the world’s largest express air cargo hub by peak-day capacity in early 2026, with 25 percent more tonnage throughput. But outside the top few cargo hubs, investments lag demand and therein lies the opportunity for private capital.

The Problem Statement: The Infrastructure Gap is a Systemic Problem

Outside the major integrator hubs, the state of air cargo infrastructure across the U.S. airport network is characterised by chronic underinvestment, legacy design, and operational inefficiency. The Airport Cooperative Research Program (ACRP) has commissioned a study to develop a Guide for Developing Airport Cargo Handling and Warehouse Infrastructure Through Public-Private Partnerships. The study is expected to document this gap, noting that cargo buildings at many airports are insufficiently sized, poorly configured with internal columns that obstruct equipment movement and undersized doors and fundamentally incompatible with modern cargo handling requirements. The gap manifests across three distinct facets.

1. Physical Facilities

Cargo terminals at mid-size and regional airports were largely designed in an era of break-bulk freight, not the high-throughput, palletised, and containerised volumes that dominate today’s market. Many lack the column-free floor plates, dock-height doors, and ramp-direct access required for efficient unit load device (ULD) handling. Cold-chain storage critical for pharmaceuticals, perishables, and biosciences cargo remains inadequate at the vast majority of U.S. airports. The pandemic-era e-commerce surge increased baseline cargo volumes at airports that were barely on the cargo map, and those airports are now handling freight at scales their infrastructure was never designed to support.

2. Operational Technology

The ACRP research (Report 143 and its ongoing supplement) confirms that cargo handling at U.S. airports “typically still relies on manual labor” and that methods “range from very manual and labor intensive to highly automated, depending largely on volume and speed of cargo handling required.” The key qualifier is that high-volume integrator hubs (FedEx Memphis, UPS Louisville) are heavily mechanised and automated, but they are the exceptions. Across the broader U.S. airport network particularly at mid-size and regional airports handling general cargo, charter freight, and smaller forwarder operations manual handling of ULDs, break-bulk freight, and loose cargo remains the norm.

This technology gap translates directly into longer dwell times, higher error rates, and diminished attractiveness to time-sensitive cargo carriers.

3. Landside Connectivity

Truck congestion remains one of the most acute bottlenecks in U.S. air cargo operations. The Government Accountability Office (GAO) reported that “more than two-thirds of the 37 stakeholders interviewed” identified challenges with warehouses, truck areas, and roadways across 11 U.S. airports[1]. Truck parking, queuing, and staging areas were specifically flagged as “too few, too small, and quite crowded.”

Insufficient truck staging areas, poorly configured internal roadways, and the absence of dedicated cargo access roads at many airports mean that landside delays frequently negate the speed advantage that shippers pay for air transport. As e-commerce fulfilment cycles shorten and last-mile delivery expectations tighten, this landside constraint has become an increasingly visible competitive liability.

Filling the Gap: The Case for Cargo P3s

The scale of the capital requirement combined with the fiscal constraints facing most U.S. airport authorities makes the case for public-private partnerships (P3s) in air cargo infrastructure both compelling and increasingly urgent. P3 models are already delivering results at airports globally that have moved decisively to adopt it.

Different P3 Models

Model 1: Ground Lease / Developer-Led (the dominant U.S. model)

How it works. The airport authority retains ownership of the land and grants a long-term ground lease typically 25 to 50 years to a private developer-operator. The developer finances, designs, builds, and operates the cargo facility at its own risk, then sub-leases space to cargo airlines, freight forwarders, and logistics operators. The airport receives a combination of upfront payments, annual base rent (often indexed or stepped), and a percentage of sub-tenant revenue. At lease expiry, the improved property reverts to the airport at no cost.

Business model. The developer earns its return through the spread between its cost of capital and the sub-lease rents it charges tenants. Typical sub-lease terms run 5–10 years, meaning the developer re-prices the facility to market multiple times within a single ground lease. The airport’s revenue is lower than if it self-developed, but it takes on zero construction or tenancy risk and preserves its capital for airside investment.

Real examples:

Salt Lake City (SLC) – AFCO (backed by Ardian Infrastructure) was selected in early 2026 as preferred bidder to develop a $50M+, 150,000 sq. ft multi-tenant cargo facility under a long-term ground lease. AFCO finances, builds, leases, and manages the facility; the airport contributes only the land and planning approvals. The facility will handle general cargo, e-commerce, and temperature-controlled operations.

Model 2: DBFOM (Design-Build-Finance-Operate-Maintain)

How it works. The airport onboards a single private partner to take on the entire project lifecycle: design, construction, financing, operation, and long-term maintenance of the cargo facility. The private partner typically holds a concession of 25-40 years and recovers its investment through user charges (throughput fees, handling charges, sub-lease rents) collected directly from cargo operators. The airport may contribute land, airside infrastructure, or enabling works, but the private partner carries the bulk of the capital risk.

Business model. This is a full-spectrum concession. The private partner’s return depends on cargo throughput it takes demand risk. In exchange, it has full operational control and pricing authority (within contractually agreed parameters). The airport benefits from a modern, purpose-built facility delivered faster and typically 15-20% cheaper than equivalent public procurement, with performance obligations enforceable through the concession agreement. The model works best at airports with strong, demonstrable cargo demand that gives the private partner confidence in the revenue forecast.

Globally, the cargo P3 market has converged on two models: ground leases and BOT/franchise concessions — not full DBFOM. The distinction matters. Under a ground lease, the developer builds speculatively and earns its return by sub-leasing to multiple tenants; the airport collects a predictable rent stream irrespective of occupancy. Under a DBFOM or concession, the private partner’s return is tied directly to cargo throughput and user charges — it carries demand risk, not just construction risk. The practical implication: concession-based models require demonstrable, bankable demand — typically underpinned by an anchor tenant commitment. Ground leases, by contrast, can be deployed at airports with emerging or unproven cargo markets, because it is the developer — not the airport authority — that absorbs tenancy and occupancy risk. For most mid-size U.S. airports exploring cargo infrastructure investment for the first time, the ground lease remains the lowest-friction entry point.

Real examples:

Though not strictly a Model 2 case study, Anchorage (ANC) NorthLink Aviation – NorthLink operates the cargo facility under a 55-year deal. With Cathay Pacific as anchor tenant and an operational target of summer 2026, NorthLink has agreed to pay a flat ground rent per square foot per year in base rent to Alaska DOT&PF. That’s a fixed, predictable payment it doesn’t fluctuate with cargo throughput, tenant occupancy, or revenue performance. NorthLink has the right to design, finance, build, and operate cargo infrastructure on the leased land.

Bankable demand in the cargo realm is very different than for a Passenger Terminal. Passenger terminals have relatively stable, diversifiable revenue (aeronautical fees, retail concessions, parking). Cargo throughput is volatile it swings with trade cycles, e-commerce surges, and carrier network decisions. That volatility makes it harder for a DBFOM concessionaire to underwrite a 25-40 year revenue forecast, and harder for lenders to finance it.

Cargo infrastructure economics favour simpler, faster structures where the developer takes real estate risk (ground lease) or operating risk (franchise concession), but not the full lifecycle bundle that DBFOM demands. A case in point is Memphis Airport. FedEx lost its air cargo transportation contract with the U.S. Postal Service, which expired on September 29, 2024.

FedEx accounts for 99% of all cargo handled at Memphis a concentration level that is essentially unprecedented at a major cargo airport. In fiscal years 2024 and 2025, FedEx handled 4.4 million and 3.5 million U.S. tons respectively. A well-structured cargo P3 transfers demand risk to the private partner. If Memphis had a concession model where FedEx paid throughput fees, the airport still gets hit by the volume decline but at least the construction capital, operating risk, and maintenance obligations sit with the concessionaire. Under a ground lease, the airport’s rent is fixed regardless of throughput (which protects it), but the airport also can’t capture upside from volume growth.

The Policy Tailwind

The current federal environment is notably supportive. The current administration has signalled a strong preference for P3 procurement models as a lever to accelerate infrastructure delivery without expanding federal outlays. Component P3s at U.S. airports covering passenger terminals, cargo facilities, consolidated rental car centres, and landside infrastructure have generated over $24 billion in private capital investment in the last decade. The Bipartisan Infrastructure Law continues to direct Airport Improvement Program (AIP) funds toward cargo-enabling projects, including apron reconstruction, taxiway access, and cargo roadway improvements that materially reduce the risk profile of adjacent private investment in landside facilities.