The Phoenix Precedent

When Phoenix Sky Harbor opened its kerb to Waymo’s fully driverless Jaguar I-PACEs in December 2023, the city made a pragmatic choice: treat autonomous vehicles (AV) exactly like every other Transportation Network Company. The existing TNC permit framework—annual vehicle permits, geofence-triggered trip logging, and a flat per-trip fee for every pick-up and drop-off—was extended to Waymo without a bespoke regulatory carve-out. That decision has proven consequential. Waymo surpassed 100,000 airport trips cumulatively by mid-2025 and now accounts for a meaningful share of Sky Harbor’s weekly TNC movements, operating 24/7 across Terminals 3 and 4.

The fee itself has followed a pre-set escalation path. Starting at $2.66 per curbside pick-up, it rose through annual increments to $5.00 in 2024. Beginning January 2025, Phoenix City Code 4-78 indexes the rate to the greater of 3% or the annual CPI-U change—placing the current effective rate at approximately $5.15 per trip. Critically, both pick-ups and drop-offs are charged, meaning a single round-trip Waymo ride to Sky Harbor generates north of $10 in airport ground-transportation revenue. With Waymo’s fleet set to roughly double once the new Magna-partnered Mesa assembly plant reaches full output—targeting an additional 2,000 Jaguar I-PACEs by end of 2026—trip volumes could grow sharply, and with them the revenue line.

Concept of Operations: How It Actually Works

The concept of operations (ConOps) for autonomous TNC service at an airport differs from human-driven ride-hail in ways that are subtle but operationally significant. In the conventional model, a TNC driver receives a ride request, enters the airport geofence, navigates to the designated pick-up zone (typically Level 1 of each terminal at Sky Harbor), waits for the passenger, and departs. Between trips, drivers stage in a surface-lot holding area—a TNC staging lot located outside the immediate terminal footprint—where they wait, engine idling, for the next dispatch.

Waymo’s ConOps eliminates the driver but introduces a different operational cadence. Vehicles are dispatched from a centralised depot—in Phoenix, the 70,000+ sq ft Chandler facility that houses fleet maintenance, cleaning, and DC fast-charging—rather than from a nearby staging lot. When a ride request is matched, the vehicle drives itself to the terminal kerb, collects the passenger, and proceeds to the destination. On a drop-off, the vehicle enters the airport, delivers the passenger curbside, and either accepts a queued return trip or repositions back toward the depot or a high-demand zone in the metro area.

This depot-centric model has three implications for airports. First, it reduces demand for on-airport TNC staging lots because vehicles are not loitering on-site between trips; they reposition algorithmically. Second, it increases the predictability of kerb dwell times—Waymo’s vehicles pull into a precise GPS-designated spot and depart once the passenger is aboard, with no circling or double-parking. Third, it shifts the compliance mechanism from driver behaviour enforcement to API-level data exchange: airports can monitor fleet movements, geofence crossings, and trip counts through a direct integration with the Waymo platform rather than relying on TNC driver app pings.

The Fee Architecture: Curbside, Staging, and Beyond

Airport ground-transportation revenue from TNCs rests on a layered fee architecture that most airports are still adapting for autonomous fleets.

Curbside trip fees. The per-pick-up and per-drop-off charge—$5+ at Phoenix, roughly $6 at SFO—is the primary revenue instrument. SFO’s programme alone generated over $60 million from more than 10 million Uber and Lyft transactions in 2025. When Waymo launched SFO service in January 2026 (operating from the Rental Car Center Level 1 curbside via AirTrain), it was folded into the same fee schedule. The principle is straightforward: if you touch the kerb, you pay.

Staging-area access. Airports such as Sky Harbor designate TNC staging lots with 30-minute occupancy limits, enforced by geofence. Human-driven TNCs pay implicitly through the trip fee (staging is bundled), but an autonomous operator with a large captive fleet could, in theory, negotiate a standing holding-area lease—a monthly or annual rental for reserved staging capacity near the terminal. No US airport has publicly disclosed such an arrangement with Waymo to date, but the concept needs to be explored. Washington Dulles’s third kerb—a dedicated 500-linear-foot TNC pick-up lane with steel canopy—illustrates how airports are already carving out premium real estate for ride-hail, and a similar premium-access model could apply to AV staging.

Electric-vehicle charging fees. This is the frontier. Waymo’s fleet is fully electric (Jaguar I-PACE, transitioning to the Geely Zeekr), and every vehicle that serves the airport must charge somewhere. Today, Waymo charges at its own off-airport depot in Chandler, drawing power through utility partnerships with Salt River Project (SRP) and Arizona Public Service (APS). The airport collects nothing from this energy transaction. But if an airport were to install DC fast-charging infrastructure on or adjacent to the terminal—say, integrated into a redesigned TNC staging lot—it could levy a per-kWh or per-session charging fee on top of the trip fee.

Can Waymo Go Solar and Sidestep Charging Fees?

The question is commercially relevant. Waymo already procures 100% renewable energy for its fleet—purchasing over 6,200 MWh of solar and wind energy in 2022 through partnerships with NextEra Energy Resources, SRP, and Google’s clean-energy portfolio. In Arizona, the economics of behind-the-meter solar are compelling: utility-scale solar PPAs in the state run below $0.03/kWh, and commercial rooftop installations can achieve levelised costs under $0.05/kWh.

Could Waymo install its own solar canopy at a leased airport staging area and effectively zero out its charging cost? Technically, yes. A 1 MW solar carport covering a 50-vehicle staging lot in Phoenix could generate roughly 2,000 MWh per year—enough to supply approximately 150 to 200 fast charges per day at the lot. But airports control the real estate. Any on-airport solar installation would require a ground lease, utility interconnection approval, and adherence to FAA glare and obstruction standards. The airport could structure the lease so that it captures a share of the energy savings—for example, charging a per-kWh facility fee on any electricity generated on airport property, or requiring Waymo to purchase power through the airport’s master-metered utility account at a marked-up rate.

In other words, the airport’s leverage is real-estate control. Waymo can source cheap solar, but it cannot bypass the landlord. Smart airports will use this leverage to create a new revenue stream rather than simply blocking the installation. A joint-venture model—airport provides the land and electrical interconnection, Waymo funds the solar and charging hardware, and savings are shared—may prove the most durable structure.

Holding-Area Rental: The Quiet Revenue Opportunity

Today’s TNC staging lots are open-access, first-come-first-served facilities with minimal revenue attribution. But as autonomous fleets scale, airports have an opportunity to monetise staging differently. An AV operator with 200+ vehicles serving a major airport may need a dedicated, technology-equipped holding area with charging bays, vehicle-to-infrastructure (V2I) communication nodes, and cleaning stations. This looks less like a parking lot and more like a micro-depot—and it commands a different price.

Avinia Labs projects that a 50-bay AV holding area at a large US airport could generate over $2.5 million per year in lease revenue, depending on the fee structure (fixed monthly base plus per-vehicle-per-day overage, or a blended per-trip surcharge). The holding area also gives the airport operational benefits: predictable kerb arrivals, reduced terminal-road congestion, and a single point of geofence enforcement. For the AV operator, the trade-off is guaranteed proximity to the terminal—shorter deadhead miles, faster passenger pick-up, and lower energy consumption per trip.

Applications for Other Airports

SFO’s early Waymo deployment—approved in late 2025, operational from January 2026—follows the Phoenix playbook on fee parity: the same ~$6 per-trip TNC fee applies to Waymo as to Uber and Lyft. But SFO faces tighter real-estate constraints. The current pick-up location at the Rental Car Center, accessible via AirTrain, is workable but not optimal for passenger experience. As volumes grow, SFO will need to consider a dedicated AV kerb at the terminal level—and the capital investment that entails.

San Jose Mineta (SJC), which became the first California commercial airport to welcome Waymo in September 2025, and San Antonio International, which launched Waymo service in March 2026, are both at earlier stages of the curve. Their opportunity is to leapfrog Phoenix by designing AV-ready ground-transportation infrastructure from the outset: integrated charging, dedicated staging, and API-native trip-fee collection.

For mid-size US airports watching from the sidelines, the lesson from Phoenix is that early adoption generates data, and data enables better pricing. Sky Harbor’s three-year head start means it now has empirical evidence on trip volumes, kerb dwell times, peak-hour distributions, and revenue per vehicle—intelligence that will inform its next round of fee negotiations with Waymo and any competing AV operator that enters the market.

Avinia’s View

The autonomous vehicle is not a future-state planning assumption; it is a present-day operational reality at four US airports and counting. Airport operators who treat Waymo as simply another TNC are leaving revenue on the table. The trip fee is necessary but not sufficient. A comprehensive AV ground-transportation strategy should encompass curbside access pricing, dedicated staging-area leases, EV charging infrastructure (with or without on-site solar), and a digital ConOps that replaces driver-behaviour enforcement with fleet-level API integration.

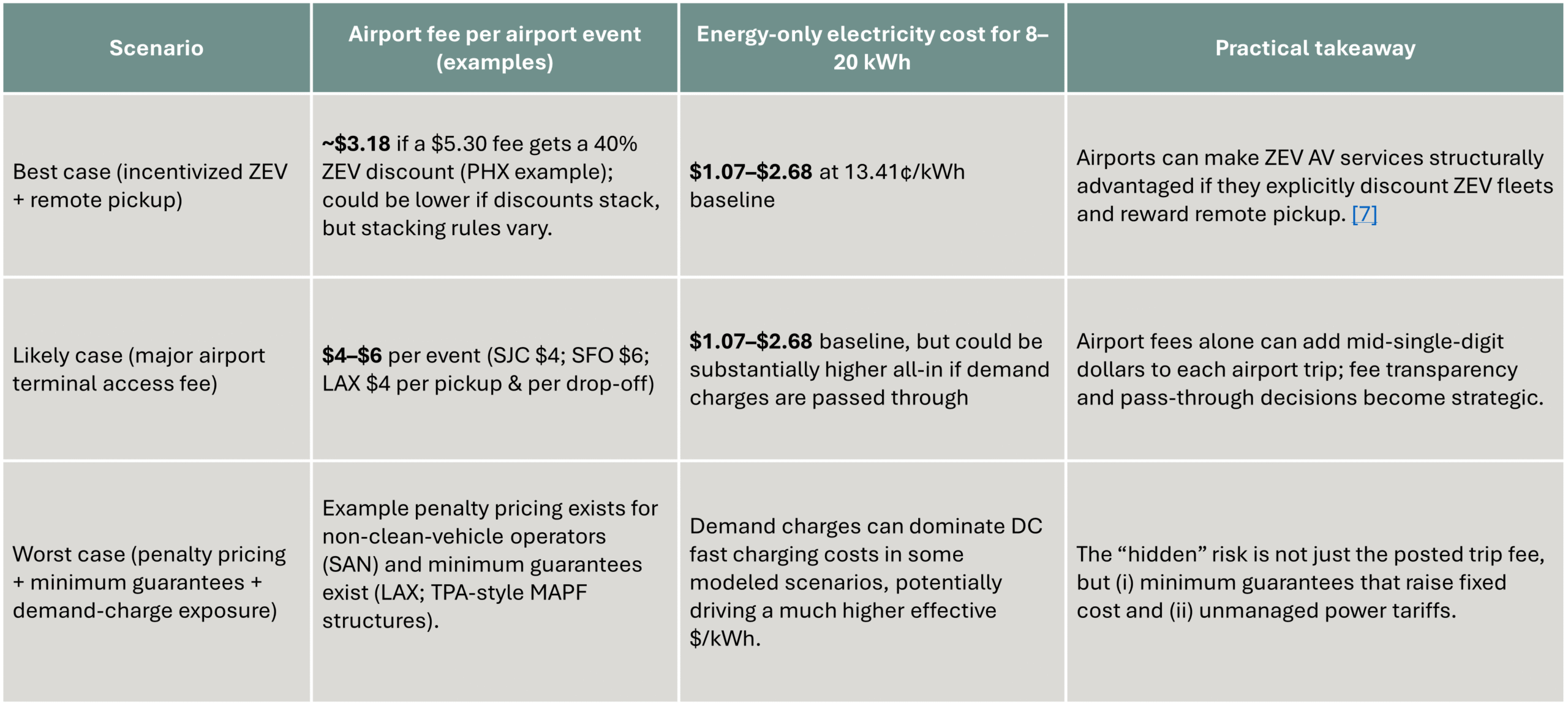

Because per-trip airport fees can be $4–$6+ per airport event in multiple large-airport examples, airport monetization can become a material portion of variable trip cost—especially for shorter airport rides or for pooled first/last-mile legs.

A simple “airport-fee + electricity” sensitivity illustrates why airports’ pricing design choices matter. (These are scenarios—actual energy use per trip and local tariffs vary.)

Assumptions (explicit):

– An “airport trip event” incurs one airport fee (pick-up or drop-off) unless the airport charges both; fee levels are taken from observed airport fee schedules.

– Incremental energy drawn for an airport ride is assumed at 8–20 kWh (range chosen for scenario planning, not a claim about Waymo’s actual consumption).

– 2025 U.S. average commercial price 13.41¢/kWh as a baseline energy-only reference; demand charges can materially increase effective cost for high-power charging.

Actionable recommendations

- Adopt a transparent two-part tariff for AV/TNC operators (airports). Combine (a) a per-event access fee (pick-up/drop-off) with (b) explicit facility rent for any dedicated staging/charging footprint—priced at market rent where required—rather than trying to overload trip fees to recover facility capex. This aligns with the self-sustainability principle and market-rent expectations for non-aeronautical leasing.

- Use differentiated pricing to manage congestion (airports). Follow the demonstrated pattern of (i) charging more for the most constrained curb space and (ii) discounting remote pickup nodes (rail stations, rental car centers) that reduce terminal curb demand. The PHX Sky Train discount model is a concrete template.

- Make electricity billing explicit and tariff-aware (airports + Waymo). If Waymo charges on-airport, both sides should specify: who is the utility account holder, whether submeters are used, whether demand charges are passed through, and whether managed charging / storage is required. Demand charges can be a dominant cost driver for fast charging.

- Bundle “amenity” costs into predictable line items (airports). Airports should separate rent from utilities and shared services (electricity, water, sewer, refuse, communications) to avoid disputes and make audit trails clean—mirroring how major airports publish utility and service charges for tenants.

- Stage access expansion using measurable service-level commitments (Waymo + airports). Where Waymo access starts limited (as described in Waymo airport-service guidance), use phased milestones tied to objective metrics: curb dwell time, incident rates, accessibility performance, and on-time pickup reliability. This makes it easier for airports to justify access and pricing decisions across stakeholders.

We estimate that a large US hub airport with a mature AV programme could generate $8 to $12 million in annual incremental ground-transportation revenue from these layered mechanisms—a substantial uplift over current TNC-only fee income. The airports that build the framework first will set the market terms. The rest will be price-takers.